Budget Update Notice: The 2026/27 Federal Budget contains proposals that may affect the information in this article. As at the date of this notice, these are proposed measures and have not yet passed into law. We are reviewing and updating our content as the legislative process progresses. If you are making a decision based on any of the matters discussed here, please contact us for advice that reflects the current and proposed position.

We are often asked if there is still any benefit to holding land in a trust for land tax purposes in South Australia.

First, it is worth noting that holding land in a company can have adverse capital gains tax implications. This is because a company does not qualify for the general 50% CGT discount (Div 115 ITAA 1997). The effect of this will be that the owner of a land-holding company will end up with an ultimate rate of capital gains tax that is double the rate that would apply if they owned the property individually or through a trust. (The interim result will likely be the company’s flat rate of 30%, but further tax will be levied when the company pays dividends to its owners.)

This usually means that people investing in property need to decide on holding the property either in their own personal name or holding it through a trust. Furthermore, when considering a trust, most people are thinking about a ‘discretionary trust’. This is because of the asset protection, succession planning and taxation flexibility associated with a discretionary trust.

This brings us to South Australian land tax.

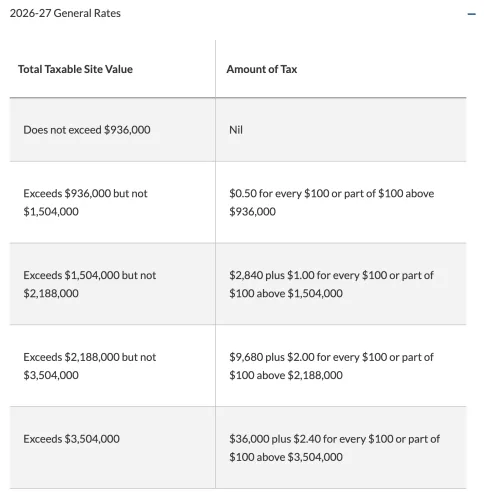

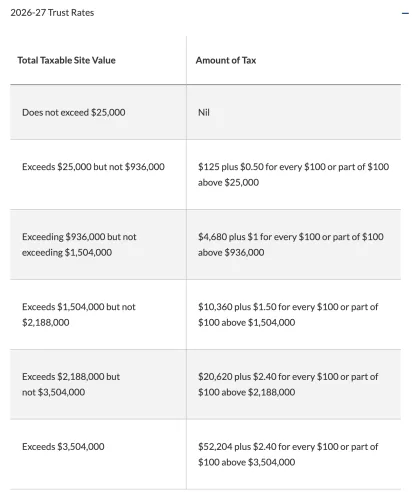

In South Australia, land tax is levied at one of two schedules of rates: The General Land Tax Rates apply to individuals and companies, and the Trust Land Tax Rates apply to trusts (other than certain limited exempt trusts).

The two schedules of rates are as follows (note: as at 2026-27 rates, which vary annually):

As you can see, the Trust Land Tax Rates are higher than the General Land Tax Rates. This is for two reasons:

- Trusts get a lower exempt threshold ($25,000 rather than $936,000); and

- Trusts pay a premium on top of each marginal rate of tax.

What this means is that you will be better off holding land in the name of an individual, provided that the individual’s total land holdings are less than $2.5 million.

However, once your total individual land holdings are more than $3,504,000, then you are better off holding any further property in a discretionary trust.

This is because each discretionary trust is treated as a separate taxpayer for SA land tax purposes. Each discretionary trust gets its own threshold (albeit to $25k), and also gets marginal rates up to 2.4% (albeit that those marginal rates are higher than the marginal rates that apply to an individual).

Let us assume that you have $5 million in total land holdings. If you hold all that land in your individual name, you will pay land tax of $77,221. However, if you held $2.5 million in your own name, and $2.5 million in a discretionary trust, then you would only pay land tax of $51,316. You could access even greater savings if the $2.5 million in additional land was spread over several trusts.

STRATEGY TIP: Put simply, once an individual has aggregate land holdings of ~$3.5 million, they will benefit from buying any further parcels of land in separate discretionary trusts.