If you’re managing wealth through a family trust and most of your beneficiaries are high-income earners, you may be grappling with how to distribute trust income without triggering the top marginal rate of tax (currently being 47%). While discretionary trusts are powerful tax planning tools, their flexibility can be limited when there’s no low-tax beneficiary to distribute to.

Enter two strategic tools: the ‘bucket company’ and the ‘banker company’. Both strategies offer high-net-worth families a way to cap tax exposure, preserve capital, and support long-term intergenerational planning. Although these terms are sometimes used interchangeably, they serve distinct purposes.

The problem: no tax-effective beneficiaries

When a discretionary trust earns income, the trustee must distribute that income to avoid being taxed at the top marginal rate (47%). If all family members are high earners, distributing income to them personally results in the top tax rate applying to the trust’s income. That’s where corporate beneficiaries come in.

What is a bucket company?

A bucket company is a company that is a beneficiary of your family trust. Its core purpose is to act like a ‘bucket’ for excess trust income, capping tax on this income at the company rate (currently 25% to 30%, depending on the size of taxpayer and type of income, i.e. business or investment). The trust distributes income to the bucket company, which:

- Pays tax at a flat company rate; and

- Retains the funds; or

- Loans them back to the trust or family members via Division 7A-compliant loans.

This strategy defers personal tax and gives the family time to manage cash flow, reinvest retained earnings, and eventually distribute franked dividends.

Key use: This strategy is best utilised for annual income smoothing and family cash flow management.

Does a bucket company sound like the right strategy for your discretionary trust distributions? We can help you establish a company and ensure loans are Division 7A compliant to maximise your benefits. Call us on 1300 654 590 or email us.

What is a banker company?

A banker company often begins as a bucket company, but over time, it evolves into the family’s investment and lending hub. It:

- Accumulates retained profits from trust distributions;

- Invests in term deposits, property, equities, or private business ventures;

- Lends funds to other companies within the family group, usually on secured terms; and

- Lends funds to family members or related trusts on commercial terms (usually under Division 7A); and

- May pay franked dividends strategically now and in future tax years.

Think of it as a long-term family ‘treasury’, managed like a corporate ‘bank’ – controlling the movement of funds across generations, preserving control, and smoothing income flows.

Key use: This strategy is best utilised for wealth accumulation, strategic lending, and succession planning.

Will a banker company be the right solution for you? We can help you decide. Call us on 1300 654 590 or email us.

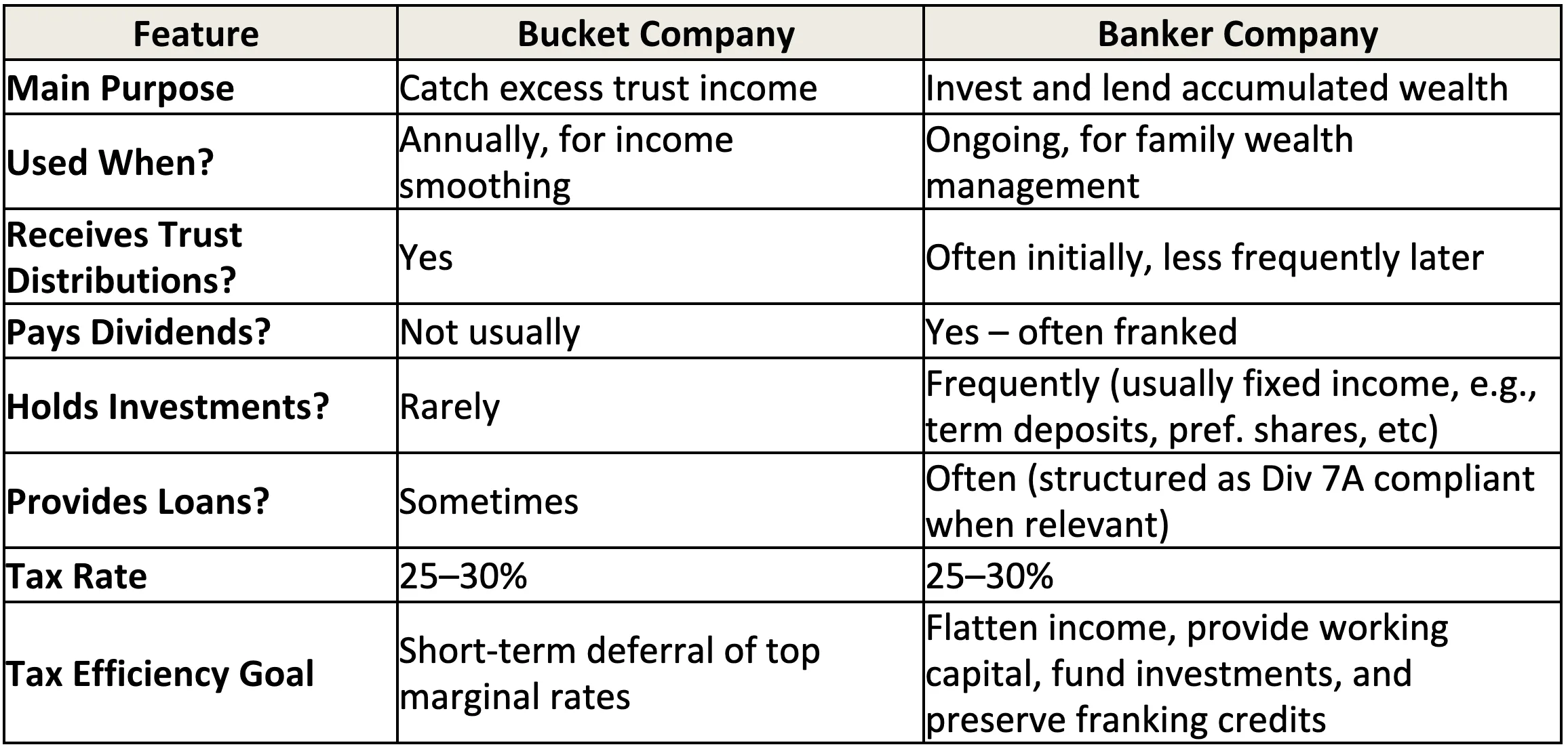

Bucket company vs Banker company

To help synthesise the difference betweent these two strategies, we have developed this comparison table.

Risks and planning considerations

While bucket and banker companies can unlock significant benefits for families managing wealth through trusts, they require careful oversight and expert structuring. These entities exist within a tightly regulated tax environment, and even small missteps can trigger large and unexpected tax liabilities or undermine asset protection strategies.

Here are some of the key risks and considerations:

Division 7A compliance

We’ve mentioned ‘Division 7A‘ a few times in this article. When a private company lends money to shareholders or their associates (including back to the family trust) Division 7A of the Income Tax Assessment Act 1936 may deem the loan a taxable dividend unless it is properly structured. To avoid this, loans must be documented in writing and comply with ATO-set minimum interest rates and repayment terms. Failure to meet the annual minimum repayment requirement results in the unpaid amount being treated as a deemed unfranked dividend.

Management of franking credits

Banker companies often accumulate franking credits through tax paid on trust distributions and investment income. These credits are a valuable tax asset and must be preserved and used strategically. Improper or mistimed dividend declarations can result in franking credit wastage. Coordinating the timing of dividends with beneficiaries’ tax profiles can improve overall outcomes.

Trust deed compatibility

Not all trust deeds allow for distributions to a company. The trust deed must be reviewed to ensure that the company is validly appointed as a beneficiary and that income streaming rules are compatible with the intended tax outcomes. Invalid distributions can lead to penalties.

Asset protection and succession planning

As retained earnings accumulate in the company, its shares become increasingly valuable. If those shares are owned personally, they may be exposed to family provision claims, estate disputes, or family law risks. Shares should ideally be held by another discretionary or testamentary trust, and succession plans should clearly deal with control and beneficial entitlements.

Base rate entity status and passive income limits

To access the lower company tax rate, the company must qualify as a Base Rate Entity. This currently requires turnover under $50 million and no more than 80% of income from passive sources. Companies with significant investment income, either directly or indirectly through trusts, will likely lose the concessional rate and affect the value of franking credits.

Yes, there is a lot to think about when utilising one of these strategies. For that reason, we always recommend seeking appropriate professional advice before implementing a bucket company or banker company strategy.

We can advise you on structuring your investments. Call us on 1300 654 590 or email us.

The bottom line

Used well, a bucket company and banker company form part of the fabric of a tax-efficient family wealth strategy. While a bucket company helps solve immediate tax pressures, the banker company supports generational wealth building, allowing a family to lend, invest, and distribute capital in a controlled, tax-effective way.

At ADLV Law, we help families structure their trusts, companies, and loan arrangements to ensure the balance between tax efficiency, legal compliance, and long-term planning is struck just right.

Call us on1300 654 590 or email us to speak to one of our estate and business structuring specialists.

The information contained in this post is current at the date of editing – 29 October 2025.