Below is Chapter 7 of our ‘Private Ancillary Funds’ booklet. To read the other chapters of our booklet, click the links below:

- Chapter 1 – Giving back to the community

- Chapter 2 – Brief history

- Chapter 3 – An overview of ancillary funds

- Chapter 4 – What is a PAF?

- Chapter 5 – Who can be a trustee of the PAF?

- Chapter 6 – How are PAFs regulated?

- Chapter 8 – Governance

- Chapter 9 – Winding up a PAF

- Chapter 10 – Common questions about PAFs

- Chapter 11 – Are they a good option for you?

- Chapter 12 – Overview of a PAF

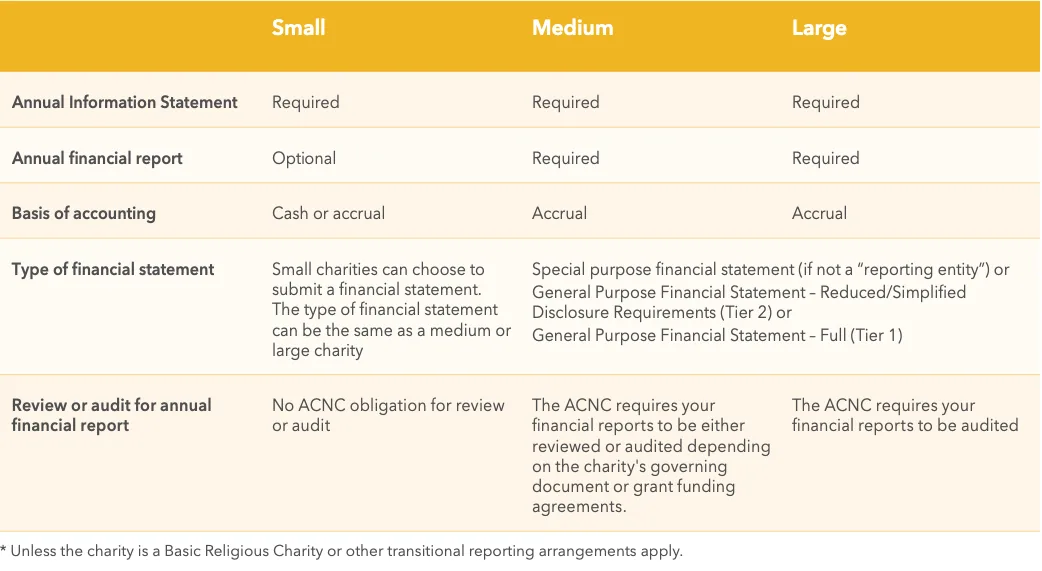

What are the reporting requirements for a PAF?

A PAF must report on its activities each year. The type of reporting required is dependent on the size of the PAF. Required reports will be an Annual Information Statement, which must be lodged with the ACNC annually, plus an annual financial report (if required). A PAF that is a small charity only needs to lodge the Annual Information Statement, whereas medium and large charities must also provide financial reports.

Refer to the table below for a summary:

• Small charities are those with annual revenue under $500,000

• Medium charities are those with annual revenue of $500,000 or more, but under $3 million

• Large charities are those with annual revenue of $3 million or more.

To download a PDF of our booklet, enter your email below.

The information contained in this post is current at the date of editing – 1 April 2026.