I don’t normally write about Budgets.

That is partly because I ceased to understand how the “Economy” was supposed to work shortly after finishing my Economics/Commerce degree about 30 years ago.

But what I do understand is the structures that Australian families and business owners use to protect what they have worked for: the family trust that holds the farm or the business, the SMSF to self-fund their own retirement, the investment property designed to replace a government pension, the SME business built over twenty plus years that has helped hundreds of employees build their own lives. This Budget touches directly on all of these.

The ‘textbook economy’ and the ‘Australian economy’ I have watched in practice over the past 30 years are not the same animal.

The textbook version says countries get richer by becoming more productive, more complex, more innovative and more open to investment. The Australian version increasingly says: dig things up, sell houses to each other, borrow against them, regulate everything else, and then wonder why young people cannot see a future.

That is the context in which this Budget matters.

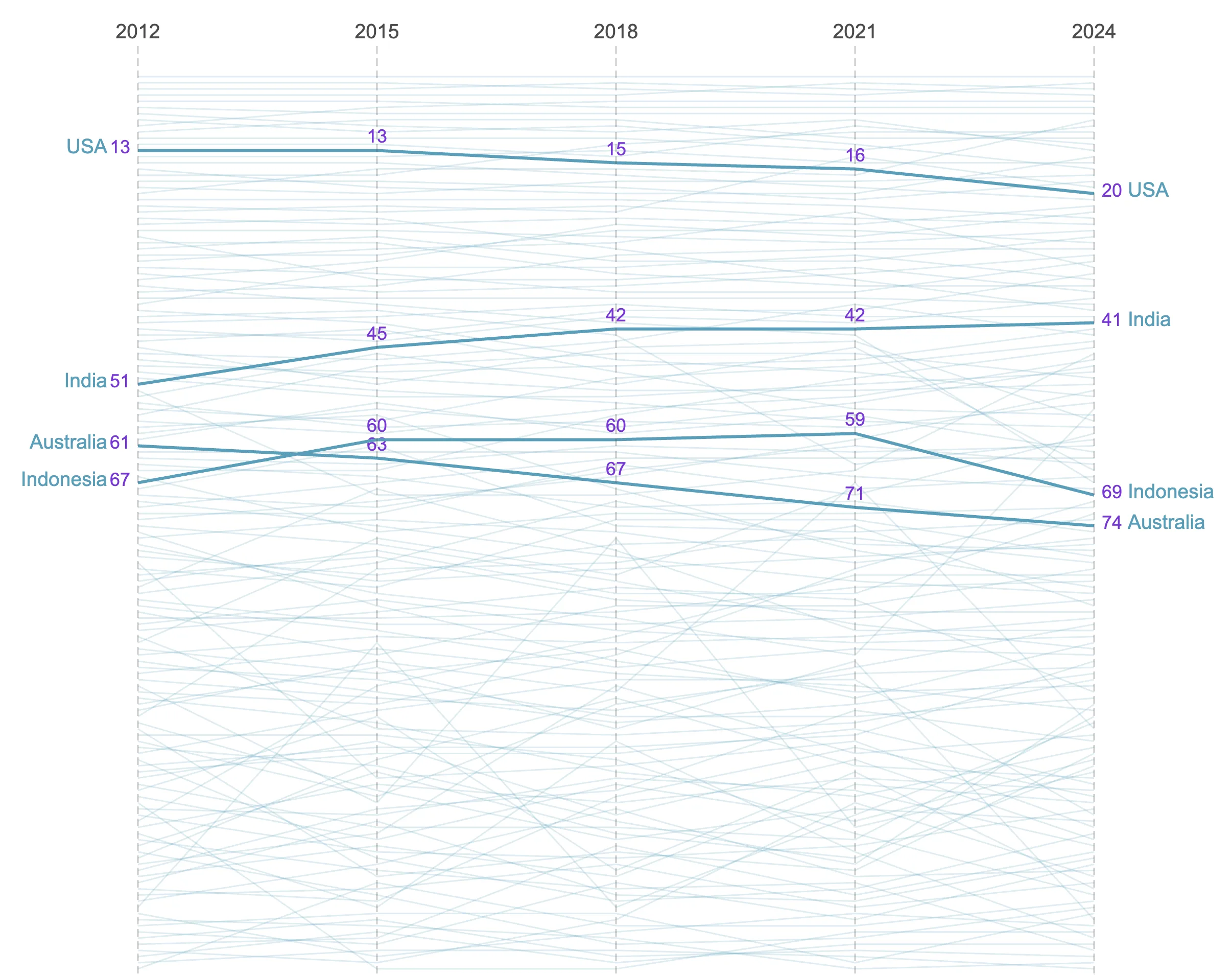

Australia is still a wealthy country. But wealth is not the same thing as productive capacity. Over 65% of our ‘wealth’ is in our unproductive homes. On ‘economic complexity’, being the sophistication and diversity of what a country can make and sell, Australia remains an outlier among advanced economies (in a bad way).

The Harvard Atlas currently ranks Australia 74th of 145 countries. Below Indonesia, India and Columbia. This ranking is better than some earlier rankings after a methodology recalibration, but still a poor result for a country that thinks of itself as advanced.

Source: Harvard Atlas. Growth Lab calculations based on HS 2012 classification and 2024 trade data.

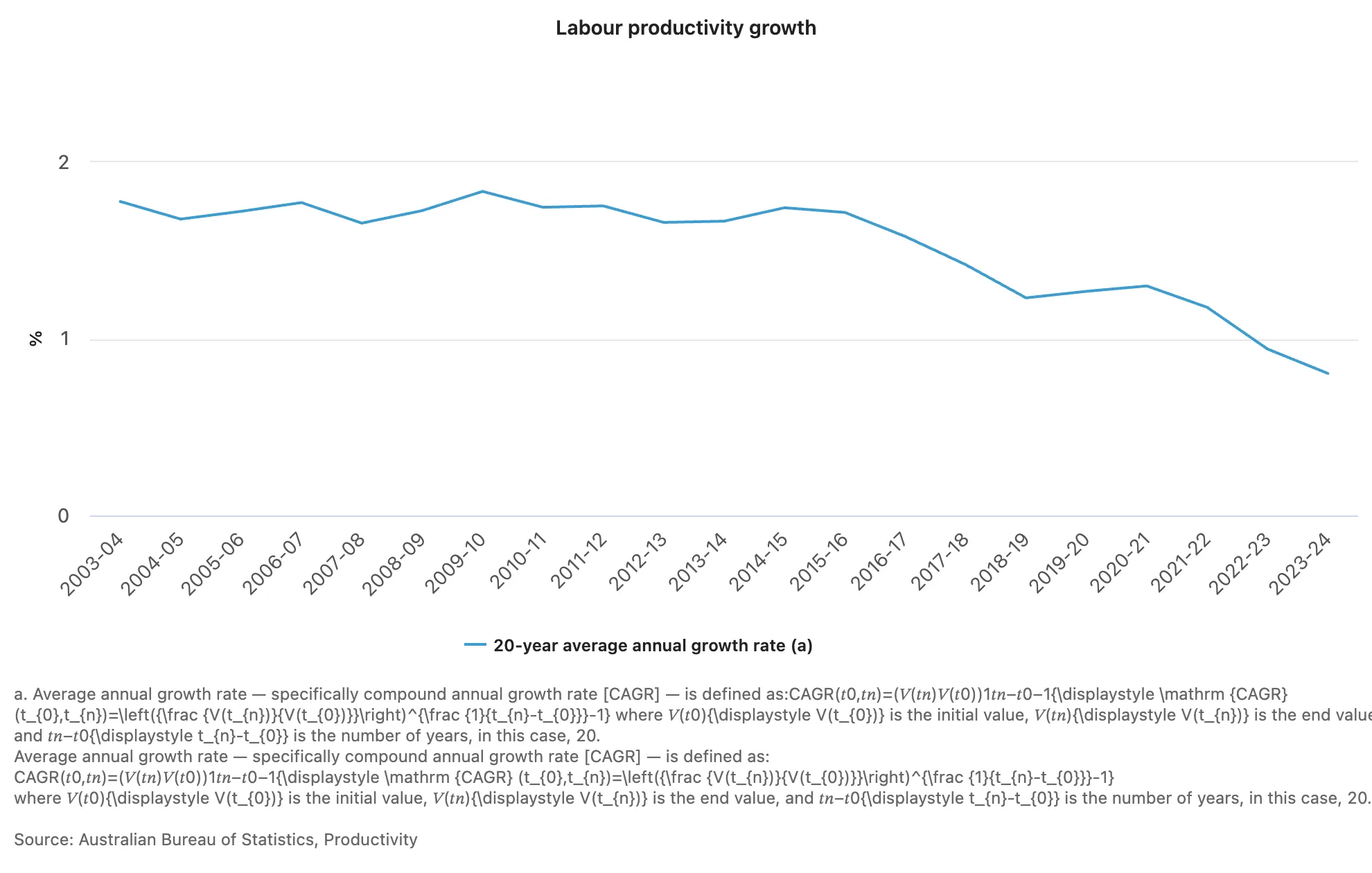

Productivity is not a ‘nice to have’, or something capitalists extract value from. Productivity is what we make, divided by how many of us there are. Productivity = Standard of Living.

Productivity is the long-term source of wages, profits, public services and living standards. The Productivity Commission and Parliamentary Library have both pointed to Australia’s recent productivity performance as among the weakest in around 60 years. Think 1970s – orange shag carpet halfway up your walls. That matters because productivity is the difference between a country that can afford its promises and a country that funds its promises by borrowing from the future.

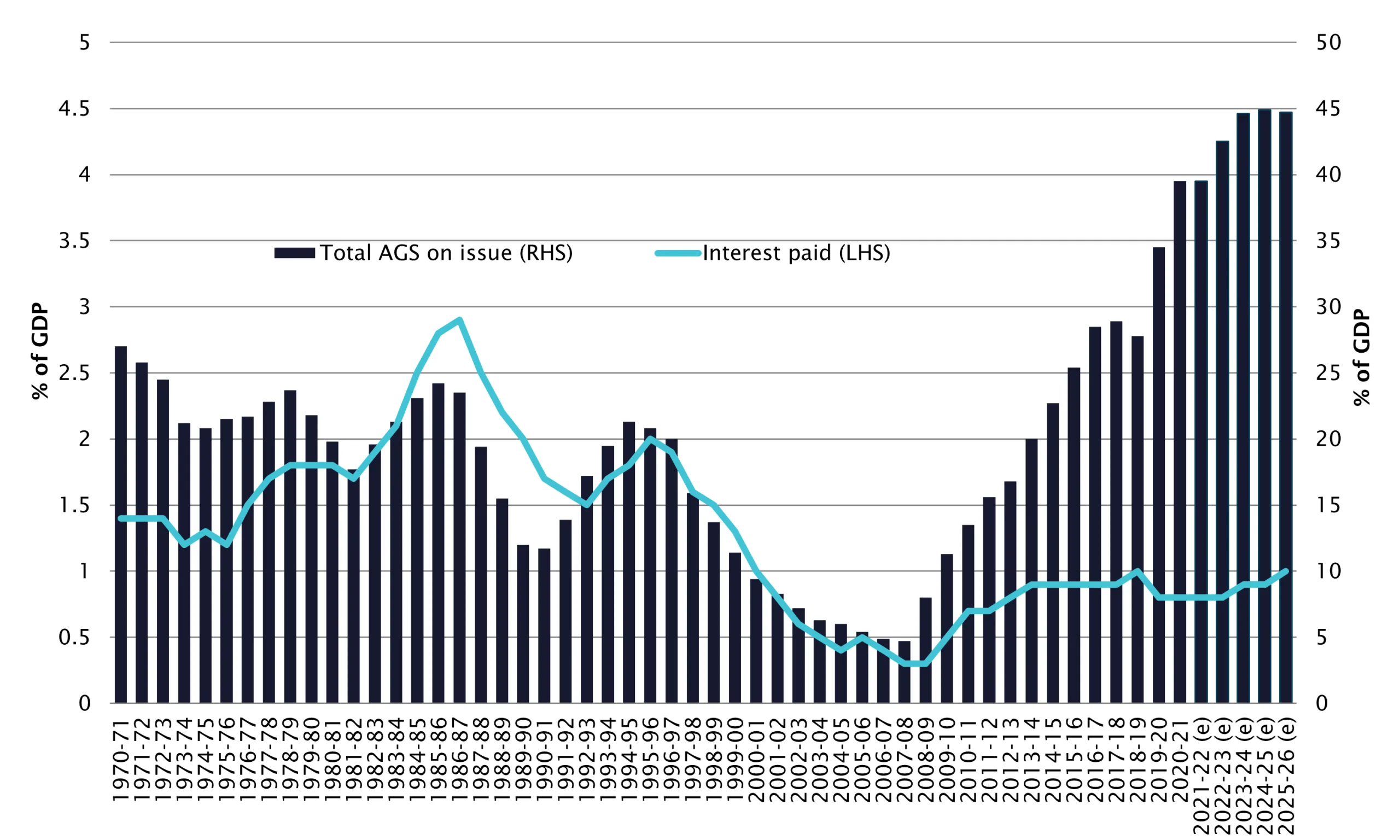

Public sector borrowing…

Source: Australian Government, Budget Strategy and Outlook: Budget Paper No. 1: 2022–23, p.348.

In 1986, when Paul Keating warned that Australia risked becoming a banana republic, we still had a domestic car industry, a broader manufacturing base, more fuel refining capacity and a clearer sense that production mattered. Today, car assembly is gone, domestic oil refining has been reduced to two major refineries, and manufacturing sits at around 5.5% of GDP. We do still make things here. But we do not make enough, and we certainly do not make enough complex things.

We are told this is because we are an “advanced economy” and have moved up the value chain.

Really?

Germany makes cars. South Korea makes cars, ships, batteries and electronics. Advanced economies do not become advanced by giving up on production. They become advanced by making harder things, better.

Meanwhile, more than one-fifth of Australia’s export income still comes from coal, gas and oil, in some years this number gets closer to a quarter. I am not a romantic about coal. I am not arguing for a permanent fossil-fuel economy. But reality has a habit of intruding. If fossil fuels are paying for a large part of our imported cars, computers, white goods, aircraft, machinery and consumer goods, then abolishing those export earnings without replacing them is not moral seriousness. It is theatre.

The real economy is thin. The property economy is obese.

Over the past few decades, Australia has become very good at three things: exporting minerals, importing finished goods, and selling increasingly expensive houses to each other using bank debt.

That is not capitalism in the heroic sense. That is not Schumpeterian creative destruction. That is not a nation of entrepreneurs building the future.

It is a leveraged land economy with a tax system and a bloated public sector attached.

The problem is made worse by market concentration. Research by Andrew Leigh and Adam Triggs found that across 481 Australian industries, the largest four firms controlled 36% of the market on average, with some industries far more concentrated. In supermarkets, the ACCC has put Woolworths and Coles at about 67% combined market share.

So we have a strange hybrid economy: not especially productive, not especially complex, not especially competitive, but very expensive.

That is the world into which this Budget lands.

Some of the Budget’s instincts are understandable. Housing has become absurd. Negative gearing has helped pour more money into established residential property. Young Australians are being asked to compete against leveraged investors, dual-income households, bank balance sheets and the tax system itself.

Servicing a new mortgage now consumes about 45% of a median household’s pre-tax income, up from about 26% in September 2020. That is not a housing market. That is a generational extraction machine.

So yes, reform is needed.

Quarantining interest deductions against future property income would have been a serious reform. With proper grandfathering or tapering, it would have been politically difficult but economically defensible.

Replacing the 50% CGT discount with indexation also has logic. The 50% discount has always been a blunt instrument. Indexation is conceptually cleaner: tax real gains, not inflation. For long-term investors, particularly in a higher-inflation world, indexation may often be fairer than the discount.

Those two reforms would have been enough.

But the Budget does not stop there.

From 1 July 2027, it proposes replacing the 50% CGT discount with indexation and imposing a minimum 30% tax on capital gains. Negative gearing would be limited to new builds for assets acquired after Budget night. From 1 July 2028, discretionary trusts would face a minimum 30% tax, paid by the trustee, with non-refundable credits for many beneficiaries.

This is where reform turns into ideology.

Investment income should be taxed. Of course it should. But investment income is not the same as wages. Investment involves risk, delay, uncertainty and the deferral of current consumption. When people invest, they do not spend today. They put capital at risk in the hope of a future return.

That is not a vice. It is the behaviour a low-productivity country should be encouraging.

The minimum 30% tax on capital gains is especially strange because it hits the very moment when a person may no longer have high ordinary income. A person can save and invest for years, retire, realise a gain, and then be told that the tax system will not allow their lower marginal rate to matter. The Budget papers present this as fairness. I see it as a penalty on patience.

The trust changes are even more concerning.

Yes, discretionary trusts can be used to split income. Yes, some arrangements are artificial. Yes, bucket company structures and circular distributions deserve scrutiny.

But discretionary trusts are not merely tax toys for the rich. They are one of the main flexible business and investment vehicles used by Australian families and SMEs. They are used for asset protection, succession planning, family investment, business risk management and intergenerational ownership.

The Government’s own material says around 350,000 active small businesses operate through discretionary trusts, while also saying most small businesses will not be affected in any given year. That is meant to be reassuring. It is not. It tells us that a very large number of real business structures will now need advice, modelling and possibly restructuring, even if they ultimately fall outside the measure.

That is how uncertainty works. It taxes people before the tax applies.

The better approach would have been targeted reform. If the concern is artificial income splitting, attack artificial income splitting. If the concern is unpaid present entitlements or corporate beneficiaries, deal with those. If the concern is distributions to people who receive no real economic benefit, use an economic benefit test.

We already know how to design more precise rules. We just prefer the drama of blunt ones.

The legal and practical complexity should not be underestimated. The CGT transition depends on values around 1 July 2027. Treasury says there will be ATO tools and specified methods for calculating gains, but for private businesses, family entities, farms, commercial property and unlisted assets, valuation will not be a neat spreadsheet exercise. It will be a cottage industry of uncertainty.

Accountants, lawyers, valuers, banks and the ATO will spend years working out what the rules mean. In the meantime, people will delay transactions, delay investment, delay restructures, delay succession and delay risk-taking.

That is our biggest objection to this Budget.

Uncertainty kills enterprise.

It kills innovation, employment, investment and confidence. It also favours large institutions over SMEs, because big institutions can absorb complexity. They have tax departments, regulatory teams and external advisers on tap. Small business owners have Saturday mornings, Xero files and a stressed accountant.

Australia already has too much big-business capitalism and not enough entrepreneurial capitalism. We have too many oligopolies, too many government-adjacent businesses, too many consultants living off public money, and too few people building globally competitive products.

So what does this Budget do?

- It makes the small and medium business landscape more uncertain.

- It makes investment structures more uncertain.

- It makes property more uncertain.

- It makes retirement planning more uncertain.

And it does this while raising comparatively modest amounts of revenue in the context of the total Budget, (a total of around $8 billion for the CGT, investment and trust measures, versus the additional $53 billion in increased defence spending). The Budget’s major fiscal pressures are elsewhere: NDIS growth, defence, health, aged care and interest on debt. The Government’s own materials point to very large NDIS savings targets and major defence commitments over the coming decade.

At the same time, we are loading young Australians with university debt and sending them through institutions that often seem embarrassed by the civilisation that funded them. That is my opinion, based on what I have seen through my own children’s education. But the financial side is not just opinion: vice-chancellor remuneration above $1 million is now common enough to have become a political issue in its own right.

We have young people who cannot buy houses, cannot trust the tax system to remain stable, and are educated to be cynical about enterprise, capitalism, investment and Western values. They are then told the answer is another round of government-designed ‘fairness’. Fairness in this Budget consists of moving 75,000 existing properties from one set of hands to another at the small ‘cost’ of killing off investment in 35,000 new homes (all figures taken from the Budget papers).

That is not a growth model!

It is a ‘managed decline’ model with better branding.

The Government is right about one thing: intergenerational unfairness is real. But the unfairness is not just that older Australians own houses. The deeper unfairness is that we have handed the next generation an economy with too little productive capacity, too little competition, too much property debt, too much regulation, and too little confidence in building.

First home buyers need cheaper houses. But they also need jobs. They need productive firms. They need capital formation. They need a country that rewards building something other than a negatively geared duplex.

That is why this Budget is such a missed opportunity.

It correctly identifies some symptoms: housing distortion, tax arbitrage, inequality, pressure on younger Australians.

But it misdiagnoses the disease.

Australia’s disease is not that too many people invest. It is that too much investment has been pushed into land, and too little into productive capacity. It is that the Government has waded into the economy and undermined the ‘supply side’ of the equation. The answer is not to make all investment feel dangerous across the board. The answer is to redirect investment from speculation into enterprise, and redirect Government activity from preventing all harm to promoting risk-taking and opportunity.

Quarantine established-property losses.

Move from the CGT discount to indexation.

Tighten artificial trust income splitting.

Encourage rollover relief where capital is reinvested into productive businesses.

Tax long-term gains more intelligently than short-term speculation. Maybe something like taper relief?

Make it easier to build, employ, export, manufacture, research, commercialise and compete.

Above all, stop treating every private investor, family business and discretionary trust as though they are guilty until proven otherwise.

Australia does not have many swings left.

If we cool the property market before rebuilding the productive economy, we may get what many people say they want: lower house prices.

But then we will discover the more important question.

What is left underneath?

On a more optimistic note, these are proposed changes, not law. The measures will be contested, scrutinised, and likely amended through the legislative process.

Our role as your advisers is to stay at the forefront of these changes. We will continue to help you understand the current landscape, the proposed changes, and the planning options available. Acting with urgency does not mean acting rashly.

The current landscape does not favour enterprise or productive investment, and the proposed changes make this harder still. Nevertheless, we continue to stand fiercely by the side of our community’s entrepreneurs and family businesses, as they continue to invest and take risks for the betterment of our economy and broader society.

– Andrew Andreyev, 2026

The information contained in this post is current at the date of editing – 25 May 2026.